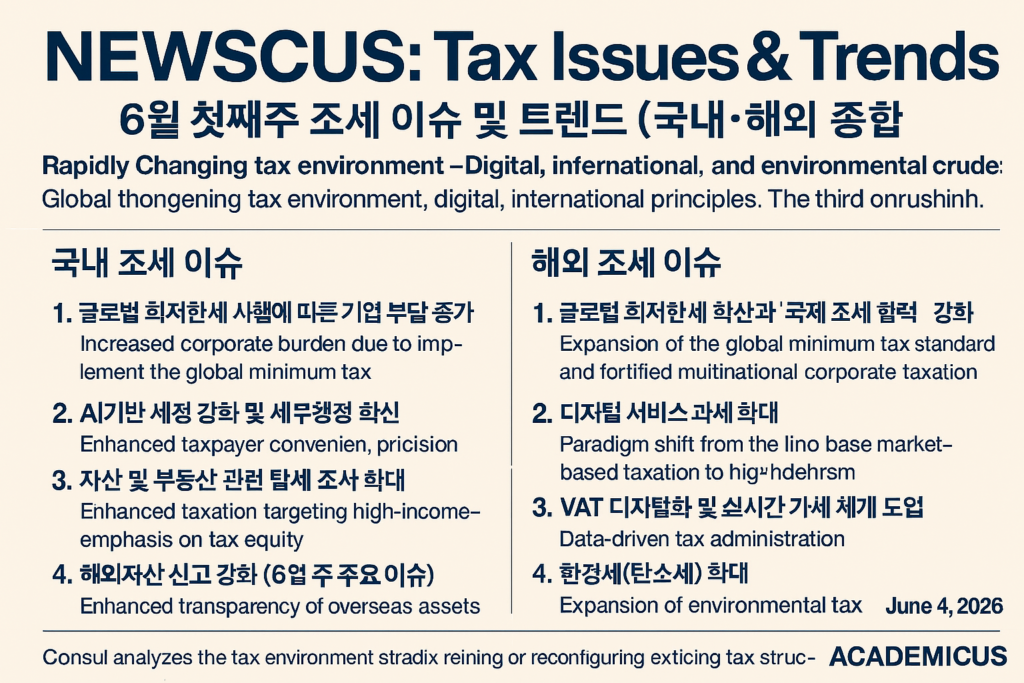

6월 첫째주 조세 이슈 및 트렌드 (국내·해외 종합)

📌 Domestic Tax Issues (Korea)(국내 조세 이슈)

1. Increased Corporate Tax Burden due to the Implementation of the Global Minimum Tax(글로벌 최저한세 시행에 따른 기업 부담 증가)

With the full-scale implementation of the global minimum tax (Pillar Two), the corporate tax burden of multinational enterprises has increased. In particular, companies that had previously reduced their tax liabilities by establishing subsidiaries in low-tax jurisdictions are now subject to additional taxation, prompting a reassessment of their tax strategies.

While this policy contributes positively to improving tax fairness, it also serves as a major factor influencing corporate investment decisions and the restructuring of global business operations.

(글로벌 최저한세(Pillar 2)의 본격 시행으로 다국적 기업의 법인세 부담이 증가하고 있다. 특히 해외 저세율 지역에 자회사를 두고 세부담을 낮춰왔던 기업들은 추가 과세 대상이 되면서 세무 전략을 재조정하고 있다.

이는 조세 형평성을 확보하는 긍정적 효과와 동시에 기업의 투자 및 글로벌 사업 구조에 변화를 초래하는 주요 요인으로 작용하고 있다.)

2. Enhancement of AI-Based Tax Administration and Innovation in Tax Systems(AI 기반 세정 강화 및 세무행정 혁신)

The National Tax Service (NTS) is advancing its tax administration system by leveraging artificial intelligence (AI), with improvements in automated tax filing and more sophisticated tax evasion detection mechanisms.

In the future, taxpayers are expected to benefit from personalized filing guidance services, enabling more convenient tax compliance. At the same time, the accuracy and efficiency of tax audits are anticipated to improve significantly.

(국세청은 인공지능(AI)을 활용한 세정 시스템 고도화를 추진하고 있으며, 세무 신고 자동화 및 탈세 탐지 기능이 더욱 정교해지고 있다.

향후 납세자는 맞춤형 신고 안내 서비스를 통해 보다 편리하게 세무 업무를 처리할 수 있게 될 것으로 기대되며, 동시에 세무조사의 정확성과 효율성도 크게 향상될 전망이다.)

3. Expansion of Investigations into Tax Evasion Related to Assets and Real Estate(자산 및 부동산 관련 탈세 조사 확대)

Recently, the government has intensified investigations into high-net-worth individuals and multi-homeowners, focusing on verifying sources of funds and detecting unreported income.

In particular, cases involving disguised transfers of wealth through real estate transactions and concealed business income have become primary targets. These measures reflect the government’s strong commitment to reducing tax blind spots and enhancing tax enforcement.

(최근 고액 자산가와 다주택자를 중심으로 자금 출처 조사 및 소득 누락 검증이 강화되고 있다.

특히 부동산 거래를 통한 편법 증여 및 사업소득 은닉이 주요 조사 대상이 되고 있으며, 과세 사각지대를 줄이기 위한 정부의 강력한 의지가 반영된 조치로 평가된다.)

4. Strengthening of Overseas Asset Reporting (Key Issue in June)(해외자산 신고 강화 (6월 주요 이슈))

Reporting obligations have been strengthened, as the scope now includes not only foreign financial accounts but also overseas trusts.

This measure aims to enhance transparency regarding overseas assets in line with increased international tax cooperation and information exchange. Failure to report may result in penalties or even criminal sanctions, requiring heightened attention from taxpayers.

(해외금융계좌 신고뿐만 아니라 해외신탁까지 신고 대상이 확대되면서 납세자의 신고 의무가 강화되고 있다.

이는 국제 조세 협력 및 정보 교환 확대에 따라 해외 자산에 대한 투명성을 확보하기 위한 조치로, 미신고 시 과태료 및 형사처벌 가능성이 있어 각별한 주의가 요구된다.)

🌍 Global Tax Issues(해외 조세 이슈)

1. Expansion of the Global Minimum Tax and Strengthening of International Tax Cooperation(글로벌 최저한세 확산과 국제 조세 협력 강화)

The OECD-led global minimum tax framework has become a key policy aimed at reducing tax competition between countries and stabilizing tax bases.

As of 2026, major economies are either implementing or preparing to adopt the system, leading to stronger international tax cooperation.

(OECD 중심의 글로벌 최저한세 제도는 국가 간 세율 경쟁을 완화하고 조세 기반을 안정화하기 위한 핵심 정책으로 자리 잡고 있다.

2026년 현재 주요 국가들이 이를 도입하거나 준비 중이며, 국제 조세 협력 체계가 더욱 강화되는 흐름을 보이고 있다.)

2. Expansion of Digital Services Taxation(디지털 서비스 과세 확대)

With the rapid growth of the digital economy, countries are increasingly expanding taxation on platform companies and online services.

Taxation standards are evolving to allow countries to tax consumption even in the absence of a physical presence, resulting in structural changes to traditional international tax principles.

(디지털 경제의 급성장에 따라 각국은 플랫폼 기업과 온라인 서비스에 대한 과세를 강화하고 있다.

물리적 사업장이 없어도 소비가 발생하는 국가에서 과세할 수 있도록 과세 기준이 변화하면서, 기존 국제조세 원칙의 구조적 개편이 이루어지고 있다.)

3. Digitalization of VAT and Introduction of Real-Time Tax Systems(VAT 디지털화 및 실시간 과세 체계 도입)

In Europe, value-added tax (VAT) administration is becoming increasingly digitalized with the adoption of e-invoicing systems and real-time transaction reporting.

These changes enable real-time data collection, playing a crucial role in preventing tax evasion and strengthening revenue collection.

(유럽을 중심으로 전자세금계산서와 실시간 거래 보고 시스템이 도입되며 부가가치세 행정이 디지털화되고 있다.

이러한 변화는 거래 데이터의 실시간 수집을 가능하게 하여 탈세를 방지하고 세수 확보를 강화하는 데 중요한 역할을 하고 있다.)

4. Expansion of Environmental Taxes (Carbon Tax)(환경세(탄소세) 확대)

As part of global efforts to address climate change, carbon taxes and emissions trading systems are being expanded worldwide.

Businesses are required to bear additional costs based on their carbon emissions, which significantly impacts production structures and investment strategies.

(기후변화 대응 정책의 일환으로 탄소세 및 배출권 거래제가 전 세계적으로 확대되고 있다.

기업들은 탄소 배출량에 따라 추가 비용을 부담하게 되며, 이는 생산 구조 및 투자 전략에 영향을 미치는 중요한 요소로 작용하고 있다.)

5. Strengthening Taxation on Cryptocurrencies and Digital Assets(암호화폐 및 디지털 자산 과세 강화)

Taxation on cryptocurrency and digital asset transactions is being reinforced, significantly improving transaction transparency.

With the expansion of automated reporting systems and cross-border information sharing, the potential for tax evasion based on anonymity is gradually diminishing.

(암호화폐 및 디지털 자산 거래에 대한 과세가 강화되면서 거래 내역의 투명성이 크게 높아지고 있다.

자동 정보 보고 시스템과 국가 간 데이터 공유가 확대되며, 익명성을 기반으로 한 탈세 가능성은 점차 축소되고 있다.)

✍ Comprehensive Analysis(종합 분석)

The current tax environment represents not merely an adjustment of tax rates, but a structural transformation occurring across taxable items, taxation methods, and administrative systems simultaneously.

(현재 조세 환경은 단순한 세율 조정이 아니라, 과세 대상, 방식, 행정 시스템까지 전반적인 변화가 동시에 진행되는 구조적 전환기이다.)

👉 Key Trends(핵심 흐름)

- Digitalization → Real-time taxation(디지털화 → 실시간 과세)

- Globalization → Enhanced international cooperation(글로벌화 → 국제 협력 강화)

- Environmental response → Expansion of new tax bases(환경 대응 → 새로운 세원 확대)

Looking ahead, tax policies are expected to become increasingly sophisticated, driven by the digital economy and international collaboration. Accordingly, both taxpayers and businesses will need to continuously adapt to the evolving tax landscape.

(앞으로의 조세 정책은 디지털 경제와 국제 협력을 기반으로 더욱 정교화될 것이며, 납세자와 기업 모두 변화하는 과세 환경에 대한 지속적인 대응이 필요할 것으로 보인다.)

- 이데일리, 「글로벌 최저한세 첫 신고…기업 세부담 증가」, 2026.06.02

- 한국세정신문, 「국세청 AI 세정 도입 및 세무조사 강화」, 2026

- 국세청, 「해외금융계좌 및 해외신탁 신고 안내」, 2026

- OECD, Secretary-General Tax Report, 2026

- World Bank, State and Trends of Carbon Pricing 2026

- Euronews, “EU Digital & Crypto Tax Proposal”, 2026.05.29

- Bloomberg Tax, “VAT Digitalization Trends”, 2026

- Tax Foundation, “Digital Services Taxes in Europe”, 2026