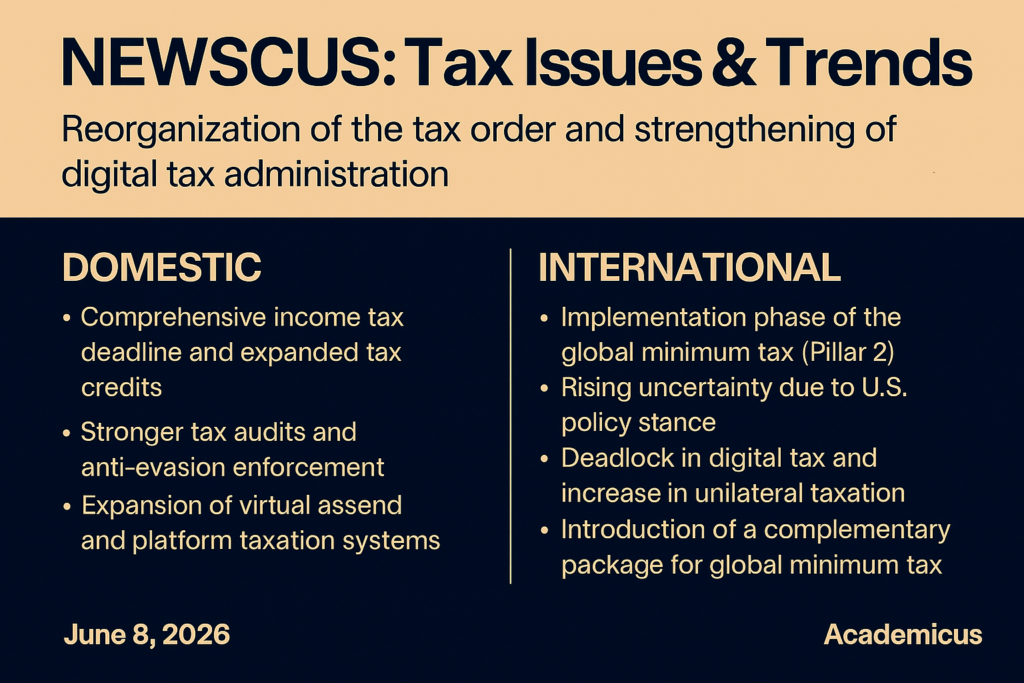

6월 둘째주 조세 이슈 및 트렌드 (국내·해외 종합)

📌 Domestic Tax Issues (Korea)(국내 조세 이슈)

1. Key Tax Event in June(6월 핵심 세무 이벤트): End of Comprehensive Income Tax Filing(종합소득세 신고 종료)

- Filing deadline for 2025 comprehensive income tax(2025 귀속 종소세 신고 마감): June 1(6월 1일)

- Payment deadline for taxpayers subject to enhanced reporting June 30(성실신고 대상자는 6월 30일까지 납부)

▶ Key Features(특징)

- Expanded tax credits, including child, rent, and marriage deductions(자녀·월세·혼인 세액공제 등 확대 적용)

- Noticeable shift in tax burden structure for sole proprietors and freelancers(개인사업자·프리랜서 세부담 구조 변화 체감)

2. National Tax Service Policy(국세청 정책): Strengthening Tax Audits & Tax Evasion Response(세무조사 & 탈세 대응 강화)

- Intensive investigations into tax evasion, including the private use of corporate vehicles(법인 차량 사적 사용 등 탈세 집중 조사)

- Expansion of the High-Value Tax Delinquent Management Task Force (approx. 10,000 individuals)(고액 체납관리단(1만명 규모) 운영 강화)

▶ Trends(트렌드)

- Simultaneous response to “everyday, close-to-home tax evasion + high-net-worth asset tax evasion”(“생활밀착형 탈세 + 고액자산 탈세 동시 대응”)

- Expansion of data-driven tax audits(데이터 기반 세무조사 확대)

3. Strengthening Taxation Infrastructure for Virtual Assets & Platforms(가상자산·플랫폼 과세 인프라 강화)

- June tax schedule(6월 세무일정): Includes mandatory submission of virtual asset transaction statements(가상자산 거래명세서 제출 의무화 포함)

▶ Implications(영향)

- Entering a full-scale phase of building a taxation system for digital assets(디지털 자산 과세 체계 본격 구축 단계)

- Accumulating data to support future expansion of taxation(향후 과세 확대 기반 데이터 축적 중)

4. Full Implementation of the 2026 Tax Reform Effects(2026 세법 개정 효과 본격 반영)

- Corporate tax rate increased by 1 percentage point(법인세율 1%p 인상) → rising corporate burden(기업 부담 증가)

- Meanwhile(대신):

- Expansion of tax exemption for childcare allowances(보육수당 비과세 확대)

- Relaxation of post-management for employment tax credits(고용세액공제 사후관리 완화)

- Expansion of tax support for start-up SMEs(창업중소기업 세제 지원 확대)

▶ “Stronger corporate taxation + expanded support for individuals and households”(“기업 과세 강화 + 개인/가계 지원 확대”)

5. Easing and Increasing Flexibility of Real Estate & Financial Taxation(부동산·금융 세제 완화 + 유연화)

- Extension of exclusion from heavy capital gains tax for multi-homeowners(양도세 중과 배제 연장 (다주택자))

- Introduction of separate taxation for high-dividend stocks(고배당 주식 분리과세 도입)

▶ Implications(영향)

- Stabilization of the real estate market(부동산 시장 안정)

- Encouragement of investment in capital markets(자본시장 투자 유도)

6. Transformation of Tax Administration Infrastructure (Digitalization & Expanded Obligations)(세정 인프라 변화 (디지털화 & 의무 확대))

- Full mandatory implementation of electronic tax invoices(전자세금계산서 전면 의무화)

- Shortened filing deadlines & expanded data submission requirements(신고기한 단축 & 데이터 제출 확대)

▶ Trend(트렌드)

- Tax administration evolving into a system of “digital + real-time management”(세무 행정 = “디지털 + 실시간 관리” 체계)

🌍 Global Tax Issues(해외 조세 이슈)

1. Entry into the Implementation Phase of the Global Minimum Tax (Pillar Two)(글로벌 최저한세(Pillar 2) 실행 단계 진입)

- In May 2026, the OECD released the Consolidated Commentary on the GloBE Model Rules(OECD는 2026년 5월 “GloBE 모델 규칙 통합 해설서(Consolidated Commentary)”를 발표)

→ Provides guidelines for consistent interpretation and implementation across jurisdictions(각국이 동일 기준으로 해석·집행하도록 가이드라인 제공) - Maintenance of the 15% effective tax rate, with clarification of details such as the application of IIR, UTPR, and QDMTT(실효세율 15% 유지, IIR·UTPR·QDMTT 적용 방식 등 세부사항 명확화)

▶ Implications(영향)

- Transition from “agreement → implementation → refinement”(“합의 → 실행 → 정교화 단계”로 전환)

- For multinational enterprises, the key task shifts from country-by-country tax rates to managing the overall effective tax rate at the group level(글로벌 기업은 국가별 세율이 아니라 “그룹 전체 유효세율 관리”가 핵심 과제)

2. U.S. Factor(미국 변수) → Increasing Uncertainty in the International Tax Order(국제조세 질서 불확실성 확대)

- The United States has pursued an independent approach in digital tax and global minimum tax negotiations(미국은 디지털세·최저한세 협상에서 독자 노선) → emergence of partial exemption structures(일부 면제(예외) 구조 등장)

- The G7 is also moving toward agreements that allow exceptions for U.S. companies(G7도 미국 기업에 예외를 인정하는 방향 합의 움직임)

▶ 결과

- 글로벌 최저한세 “완전 통일” → “국가별 변형 적용”으로 변질 가능

- 조세 주권(sovereignty) vs 국제 공조 충돌 확대

3. 디지털세(Pillar 1) 교착 + 개별 국가 확대

- Pillar 1(과세권 재배분)은 여전히 지연

- 캐나다·유럽 등은 독자 디지털서비스세(DST) 확대 시도

▶ Outcome(결과)

- Delay in multilateral negotiations(다자 협상 지연) → increase in unilateral tax measures by individual countries(국가별 unilateral tax 증가) → continued risk of trade disputes and retaliatory tariffs(무역분쟁 및 보복관세 리스크 지속)

4. Introduction of a “Complementary Package” for the Global Minimum Tax(글로벌 최저한세 ‘보완 패키지’ 도입)

- From 2026, the OECD(OECD는 2026년부터)

- Recognizes real investment incentives(실물투자 인센티브 인정)

- Expands safe harbour provisions(Safe harbour 확대)

- Introduces a side-by-side taxation system

▶ Key Change(핵심 변화)

- Shift from strengthening simple taxation(단순 과세 강화) → to a more flexible system that considers investment attraction(투자 유치 고려한 유연한 제도로 변화)

5. Structural Changes in Corporate Tax Policy (OECD Report)(법인세 정책의 구조 변화 (OECD 보고서))

- Emphasis on the impact of corporate taxation on the business ecosystem

- In particular(특히):

- High compliance costs(높은 compliance 비용) → hinder entry of startups(스타트업 진입 저해)

- Tax incentives(세제 인센티브) → may lead to bias toward large corporations(대기업 편중 가능성)

▶ Trend Summary(트렌드 요약)

- Shift from “tax rate competition”(“세율 경쟁”) → to “policy design centered on market structure and innovation impact”(“시장 구조·혁신 영향 중심의 정책 설계”)

- Google News. (2026). 대한민국 최신 뉴스.

- SBS 뉴스. (2026). 이슈 메인.

- 뉴스펌프. (2026). 2026년 정치·사회 이슈 총정리.

- 국민통합위원회. (2026). 5대 사회갈등 주요 이슈 분석 결과 발표.

- World Economic Forum. (2026). Global Risks Report 2026.

- International Monetary Fund (IMF). (2026). World Economic Outlook, April 2026.

- United Nations News. (2026). AI’s environmental costs threaten water, land and climate.

- Encyclopaedia Britannica. (2026). Major Events of 2026.