It was planned for participation in the “University (Graduate) Student Idea Short Paper Contest”, but was not submitted.(“대학(원)생 아이디어 소(小)논문 공모전” 참가를 위하여 계획하였지만 미제출함.)

[Research Overview(연구 개요)]

1. Background and Purpose of the Study(연구의 배경 및 목적)

1) Due to various socio-economic factors, the number of single-person households in Korea has been steadily increasing. As of 2021, the proportion of single-person households accounted for 12.64% of total households, the highest among all household types.(다양한 사회·경제적 요인의 영향으로 국내 1인 가구의 수가 꾸준히 증가하고 있으며, ‘21년 기준 전 체 가구 수 대비 1인 가구 수의 비율은 12.64%로 가장 높음.)

2) As of 2021, the growth rate of single-person households in Incheon was 9.49%, which is approximately 2.36 percentage points higher than that of Seoul (7.13%), where the absolute number of single-person households is the largest.(‘21년 기준 인천시의 1인가구 증가율은 9.49%로 1인 가구 수가 가장 많은 서울시의 1인 가구 증가 율인 7.13% 비해 2.36%가량 높음.)

3) The rapid increase in single-person households has led to various economic and social issues.(1인가구 수의 급속한 증가는 다양한 경제·사회적인 측면에서 문제점을 유발하고 있음.)

4) As these issues have grown, the government has introduced policies targeting single-person households and expanded support to improve their quality of life. However, there remains a need for more practical support policies and institutional improvements, particularly from an economic perspective.

(문제점이 증가함에 따라 정부는 1인 가구를 대상으로 한 정책을 마련하고, 1인 가구의 삶의 질 증 진을 위한 지원을 확대하고 있으나 경제적인 측면에서 급증하는 1인 가구를 대상으로 한 실질적인 지원 정책과 제도 개선이 필요해 보임.)

5) Following the 2013 tax reform, which converted certain income deduction items into tax credits, the earned income deduction was reduced, thereby increasing the tax burden on single-person households. Furthermore, with the rise in single-person households and the corresponding increase in temporary forms of employment, the number of taxpayers subject to income tax is expected to grow. This highlights the need for tax support policies to alleviate the tax burden on single-person households.(‘13년도 일부 소득공제 항목을 소득공제에서 세액공제로 변경하는 세법 개정으로 인한 근로소득공 제의 축소 등으로 1인 가구의 세금 부담이 늘어났으며, 1인 가구 수의 증가와 그에 따른 임시직 고용 형태의 증가로 발생하는 소득세를 부담하는 납세자의 수가 더 늘어날 것으로 예상됨에 따라 1인 가구의 세 부담 감소를 위한 세제상 지원 정책이 필요해 보임.)

6) The increase in temporary employment among single-person households has resulted in greater burdens related to voluntary tax filing, such as comprehensive income tax reporting. Although the government has introduced measures such as “mobile filing notifications” and “post-deadline refund filing guidance for personal service income earners via Hometax,” cases still occur where taxpayers fail to file within the deadline due to a lack of tax expertise, leading to missed deduction benefits and tax disadvantages. Therefore, additional measures are needed to reduce taxpayer burden and enhance compliance through improved filing convenience.(1인 가구의 임시직 고용 형태의 증가로 인해 종합소득세 신고 등 자발적인 세무 신고 부담이 발생 하고 있으며, 이에 따라 정부는 ‘모바일 신고 안내문 발송’, ‘홈택스 인적용역 소득자 종합소득세 기 한 후 환급 신고 안내’ 등의 제도를 마련하고 있으나 세무 전문 지식의 결여 등의 이유로 신고 기 한 내 신고를 하지 못해 적절한 시기에 공제 혜택을 적용받지 못하여 세제상 불이익을 받게 되는 사례가 발생함에 따라 세무 신고에 대한 납세자의 부담을 낮추고 신고 편의를 지원을 통한 성실 신고 제고를 위한 추가적인 제도 마련이 필요해 보임.)

7) In the case of personal service income (freelancers) under business income, it is often difficult to apply necessary expense deductions through proper bookkeeping. As a result, estimated reporting methods using standard expense ratios or simplified expense ratios are frequently applied, which often leads to inadequate deductions. This indicates a need for institutional improvements in this area.(사업소득 중 인적용역 소득(프리랜서)의 경우 직접 장부 기장을 통한 필요경비 공제 적용이 어려워 추계 신고를 통한 기준경비율 혹은 단순경비율이 적용되는 경우가 많아 적절한 공제가 이루어지지 못하는 경우가 빈번함에 따라 관련 제도 개선이 필요해 보임.)

8) This study aims to establish a rationale and propose directions for institutional improvement to expand tax support for single-person households through improvements in the income tax reporting system, ultimately enhancing their quality of life.(이 연구는 소득세 신고 제도 개선을 통한 1인 가구의 세제지원 확대를 통한 1인 가구의 삶의 질 증진을 목적으로 관련 논거를 구축하고, 제도 개선 방향을 제시하는 것을 목적으로 함.)

2. Scope and Methodology of the Study(연구의 범위 및 방법)

1) Definition, status, distribution, issues, and support systems of single-person households (literature review and statistical data)(1인 가구의 정의, 현황, 분포, 문제점, 지원 제도(문헌조사, 통계자료))

2) Examination of overseas support systems for single-person households and cases of improvements in income taxation systems (if necessary)(해외 1인 가구 지원 제도 및 소득세 부과 제도 개선 사례 조사(필요시))

3) Current status and issues of income tax-related systems (the scope of the study is limited to earned income and business income)(소득세 관련 제도 현황, 문제점(연구의 내용적 범위는 소득세 中 근로소득과 사업소득으로 한정함.))

4) Analysis, comparison, and calculation of the income tax burden for single-person households(1인 가구 대상 소득세 부담 현황 조사 및 비교, 계산)

5) Online survey on perception and current status of single-person households(1인 가구 대상 인식·현황 온라인 설문조사)

6) Proposals for improvements in income tax (business income) deduction/reduction systems and tax filing procedures(소득세(사업소득) 공제·감면 제도 및 신고 제도 개선 제안)

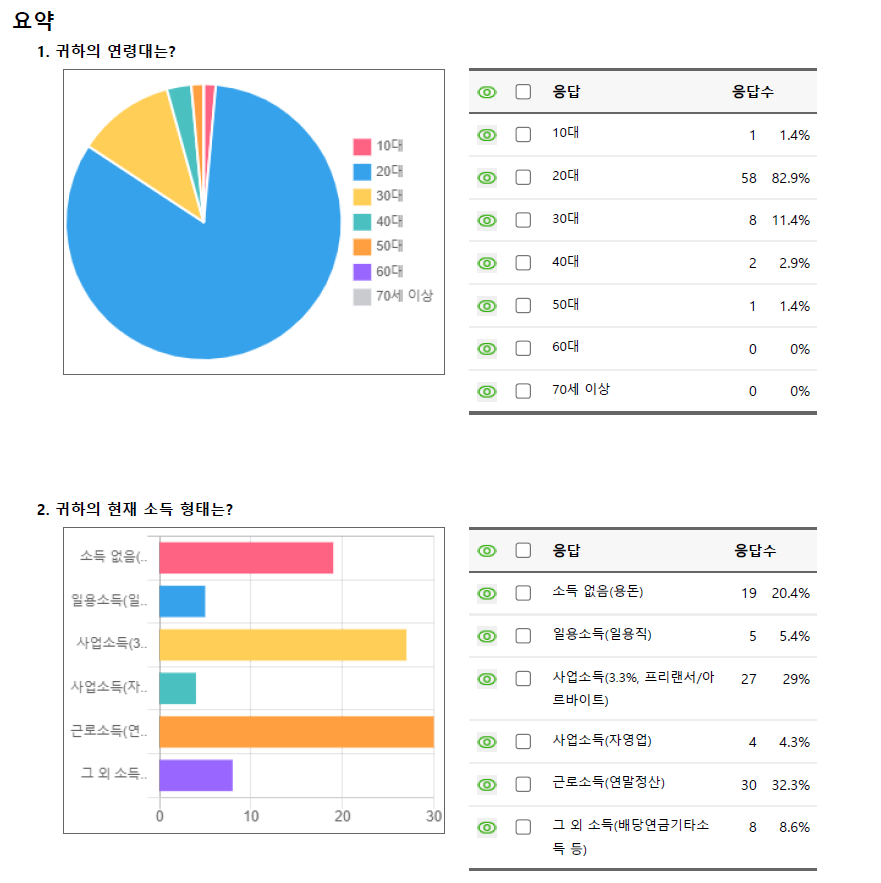

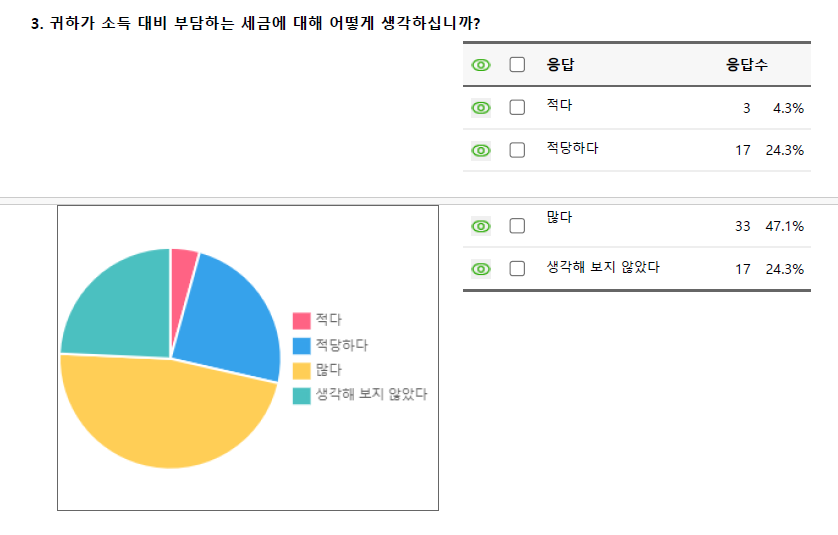

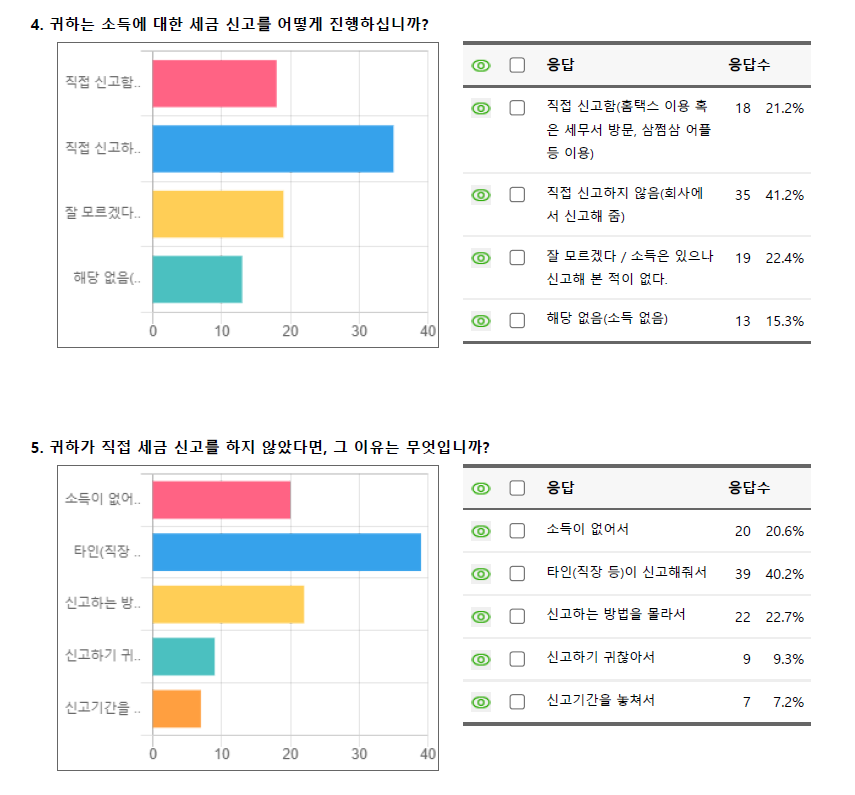

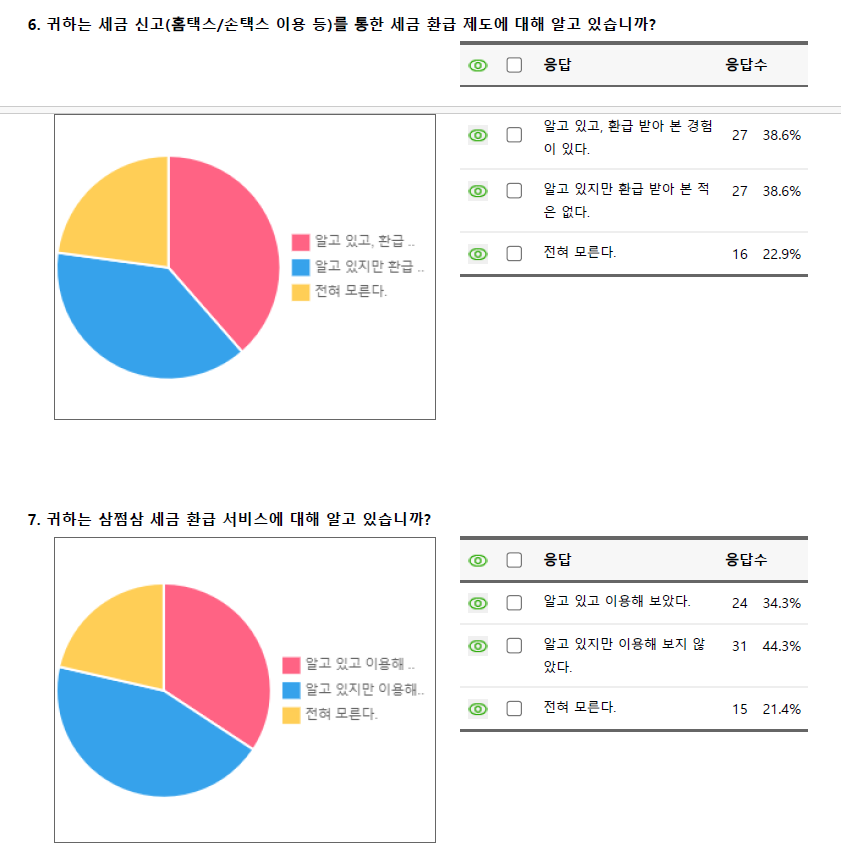

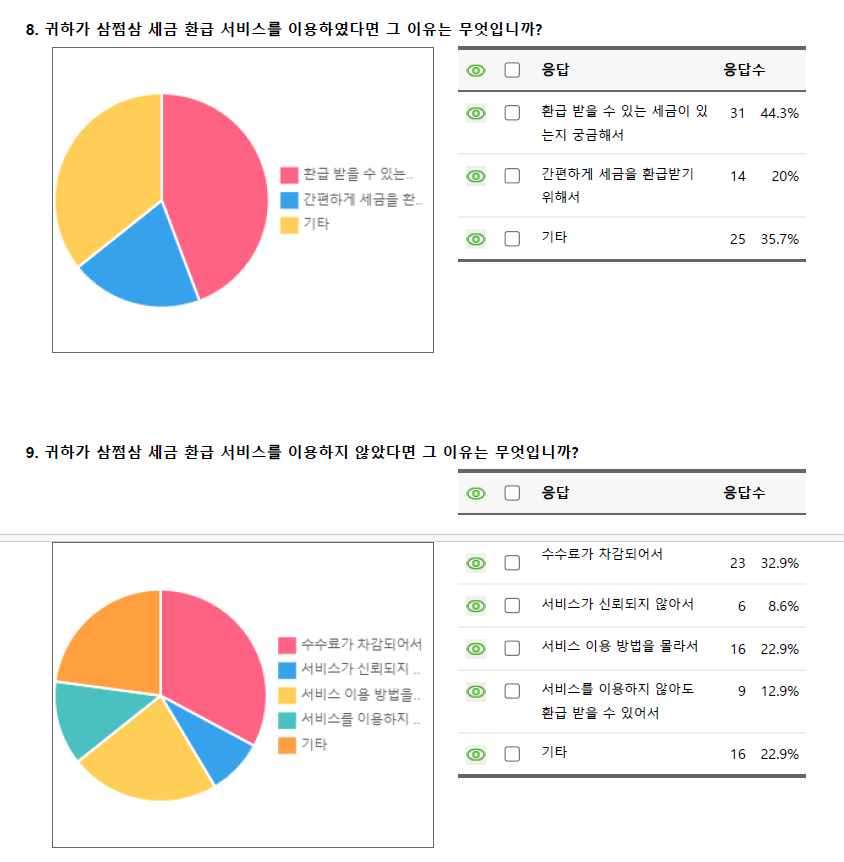

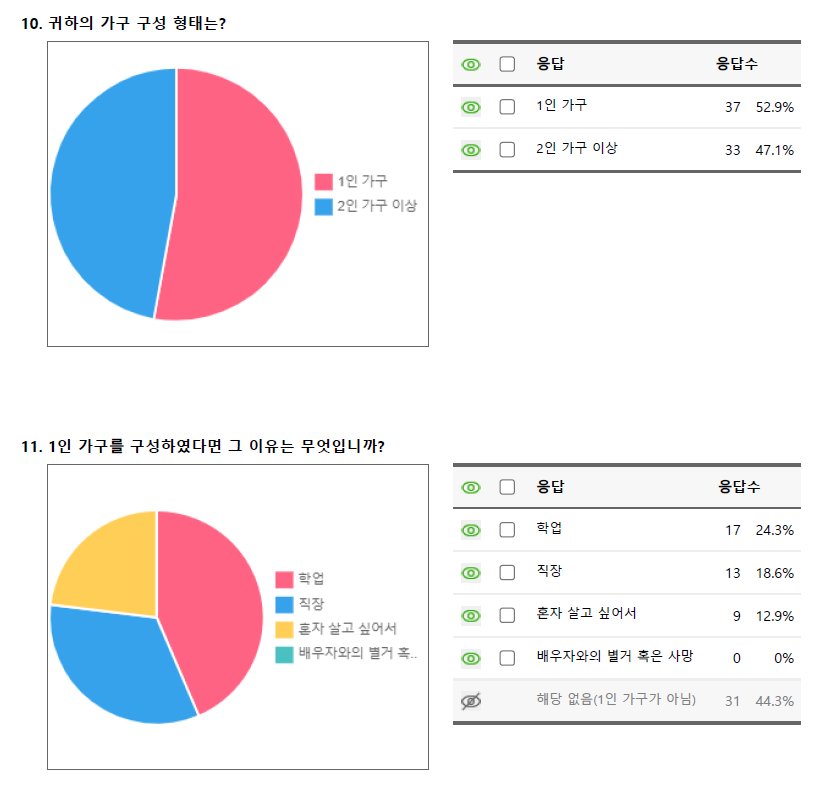

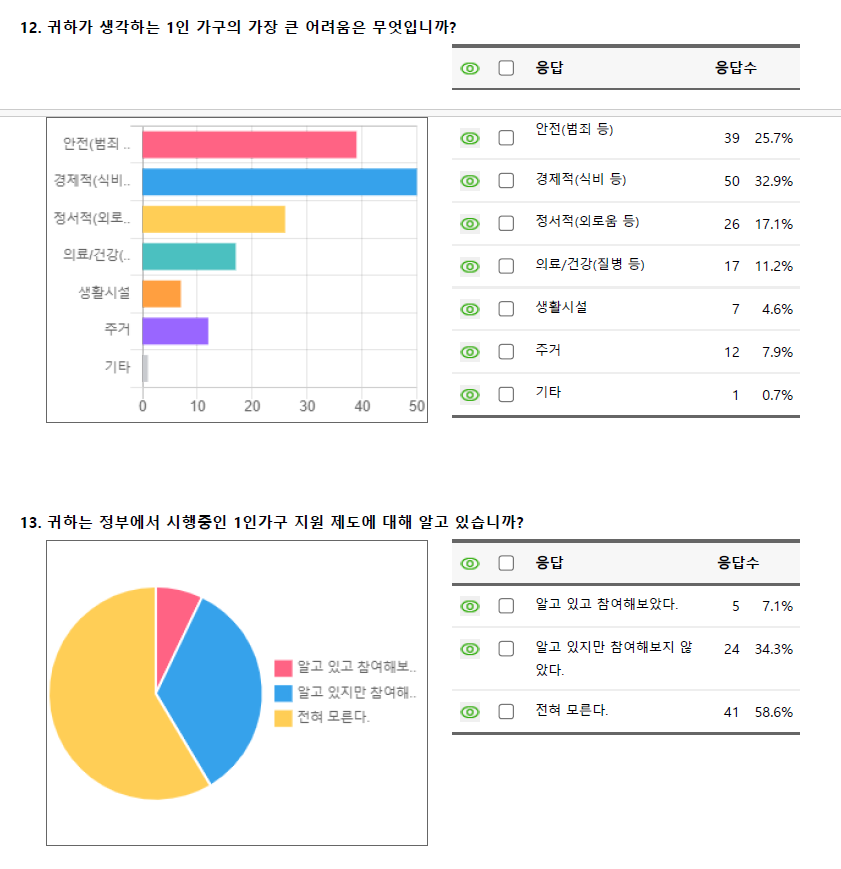

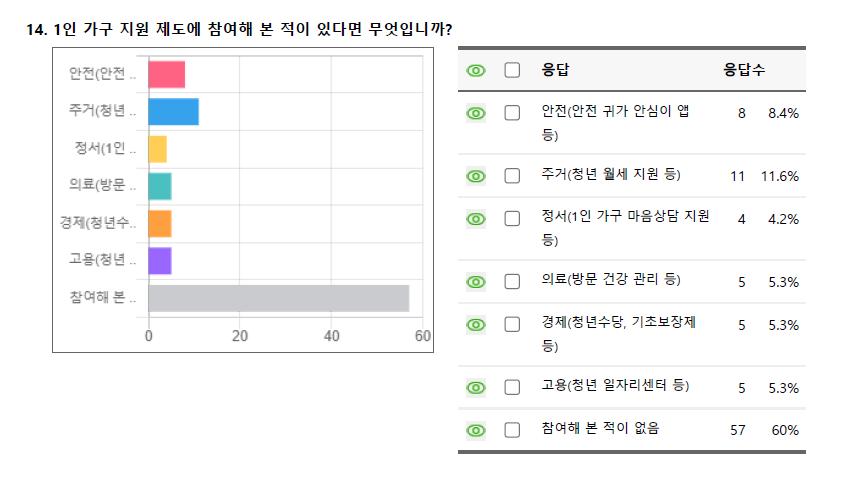

[Survey Data]